All Categories

Featured

Table of Contents

Tax obligation lien certificates, also known as tax obligation executions, certificates of acquisition, and tax sale certificates, are instruments marketed by regional, region and local governments as a technique of recuperating home tax obligation bucks regarded delinquent as a result of the building owner's failure to satisfy the debt. The issuance of tax obligation lien certificates to investors is usually done in a public auction setup where the successful bidder is established by the cheapest rates of interest stated or the highest possible quote for cash money.

6321. LIEN FOR TAXES. If any type of person responsible to pay any type of tax obligation neglects or rejects to pay the exact same after demand, the amount (including any type of passion, additional amount, addition to tax obligation, or assessable charge, together with any kind of expenses that may build up in addition thereto) will be a lien in favor of the United States upon all residential or commercial property and civil liberties to building, whether actual or personal, belonging to such person.

Division of the Treasury). Typically, the "person reliant pay any kind of tax" described in area 6321 should pay the tax obligation within ten days of the created notice and demand. If the taxpayer stops working to pay the tax obligation within the ten-day period, the tax lien occurs automatically (i.e., by procedure of legislation), and works retroactively to (i.e., arises at) the date of the analysis, despite the fact that the ten-day period necessarily expires after the assessment date.

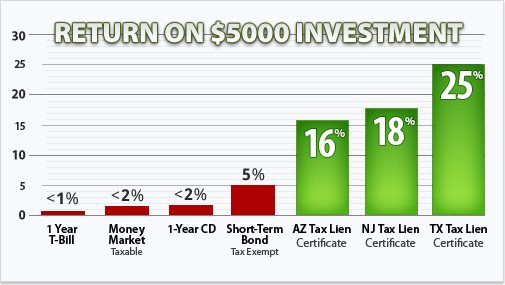

Tax Lien Investing Arizona

A government tax obligation lien developing by legislation as described over is legitimate against the taxpayer without any kind of more action by the federal government - how to do tax lien investing. The basic guideline is that where two or even more creditors have completing liens against the exact same building, the financial institution whose lien was developed at the earlier time takes top priority over the lender whose lien was refined at a later time (there are exceptions to this guideline)

The form and web content of the notice of government tax lien is controlled only by government legislation, regardless of any kind of demands of state or regional legislation. The NFTL is just a device which provides notification to interested parties of the presence of the government tax obligation lien. Therefore, the NFTL's function is to ideal and obtain top priority for the government tax lien.

Some examples consist of the liens of particular purchasers of securities, liens on particular motor vehicles, and the passion held by a retail buyer of specific individual home. Federal law likewise permits a stateif the state legislature so chooses by statuteto appreciate a higher priority than the federal tax lien relative to certain state tax liens on property where the associated tax is based on the worth of that residential or commercial property.

Are Tax Lien Certificates A Good Investment

In order to have the document of a lien launched a taxpayer needs to acquire a Certification of Launch of Federal Tax Obligation Lien. Usually, the internal revenue service will not provide a certification of release of lien till the tax has either been paid in full or the IRS no longer has a lawful rate of interest in gathering the tax.

In circumstances that get the removal of a lien, the IRS will normally eliminate the lien within one month and the taxpayer may receive a copy of the Certificate of Launch of Federal Tax Lien. The existing kind of the Notice of Federal Tax obligation Lien used by the IRS consists of a provision that provides that the NFTL is launched by its very own terms at the final thought of the statute of constraints period described above offered that the NFTL has actually not been refiled by the date indicated on the type.

The term "levy" in this narrow technological feeling signifies an administrative action by the Internal Earnings Solution (i.e., without litigating) to seize residential or commercial property to please a tax obligation responsibility. The levy "includes the power of distraint and seizure by any ways. The basic rule is that no court permission is required for the internal revenue service to perform a section 6331 levy.

The notification of levy is an IRS notice that the IRS plans to seize home in the future. The levy is the real act of seizure of the building. In general, a Notice of Intent to Levy have to be released by the internal revenue service at the very least thirty days prior to the actual levy.

While the government tax obligation lien uses to all building and rights to residential property of the taxpayer, the power to levy is subject to specific constraints. That is, particular building covered by the lien may be exempt from an administrative levy (property covered by the lien that is excluded from administrative levy may, nevertheless, be taken by the internal revenue service if the internal revenue service acquires a court judgment).

Buying Tax Liens For Investment

In the United States, a tax obligation lien might be put on a residence or any kind of other real residential or commercial property on which home tax is due (such as an empty tract of land, a boat dock, or also a vehicle parking area). Each county has differing guidelines and policies concerning what tax is due, and when it is due.

Tax obligation lien certifications are issued promptly upon the failure of the home proprietor to pay. The liens are normally in first setting over every various other encumbrance on the residential property, including liens secured by financings against the residential property. Tax obligation lien states are Alabama, Arizona, Colorado, Florida, Illinois, Indiana, Iowa, Kentucky, Louisiana, Maryland, Massachusetts, Mississippi, Missouri, Montana, Nebraska, Nevada, New Jacket, New York, Ohio, Rhode Island, South Carolina, Vermont, West Virginia, and Wyoming.

Tax obligation acts are provided after the proprietor of the property has fallen short to pay the taxes. Tax actions are released in connection with public auctions in which the residential property is sold outright. The starting quote is frequently just for the back tax obligations owed, although the scenario might differ from one region to an additional.

"Tax Action States 2024". Tax liens and tax deeds can be acquired by an individual capitalist. In the instance of tax obligation liens, passion can be earned. If the residential property is redeemed then the financier would recoup invested money, plus rate of interest due after the lien was purchased. If the residential or commercial property is not retrieved, the deed holder or lien owner has very first setting to own the building after any kind of other tax obligations or costs are due. [] 6321.

See 26 C.F.R. section 601.103(a). 326 U.S. 265 (1945 ). U.S. Constit., art.

{kind=link}

Latest Posts

Tax Repossessed Property

How To Do Tax Lien Investing

Investing In Tax Lien Certificates For Beginners